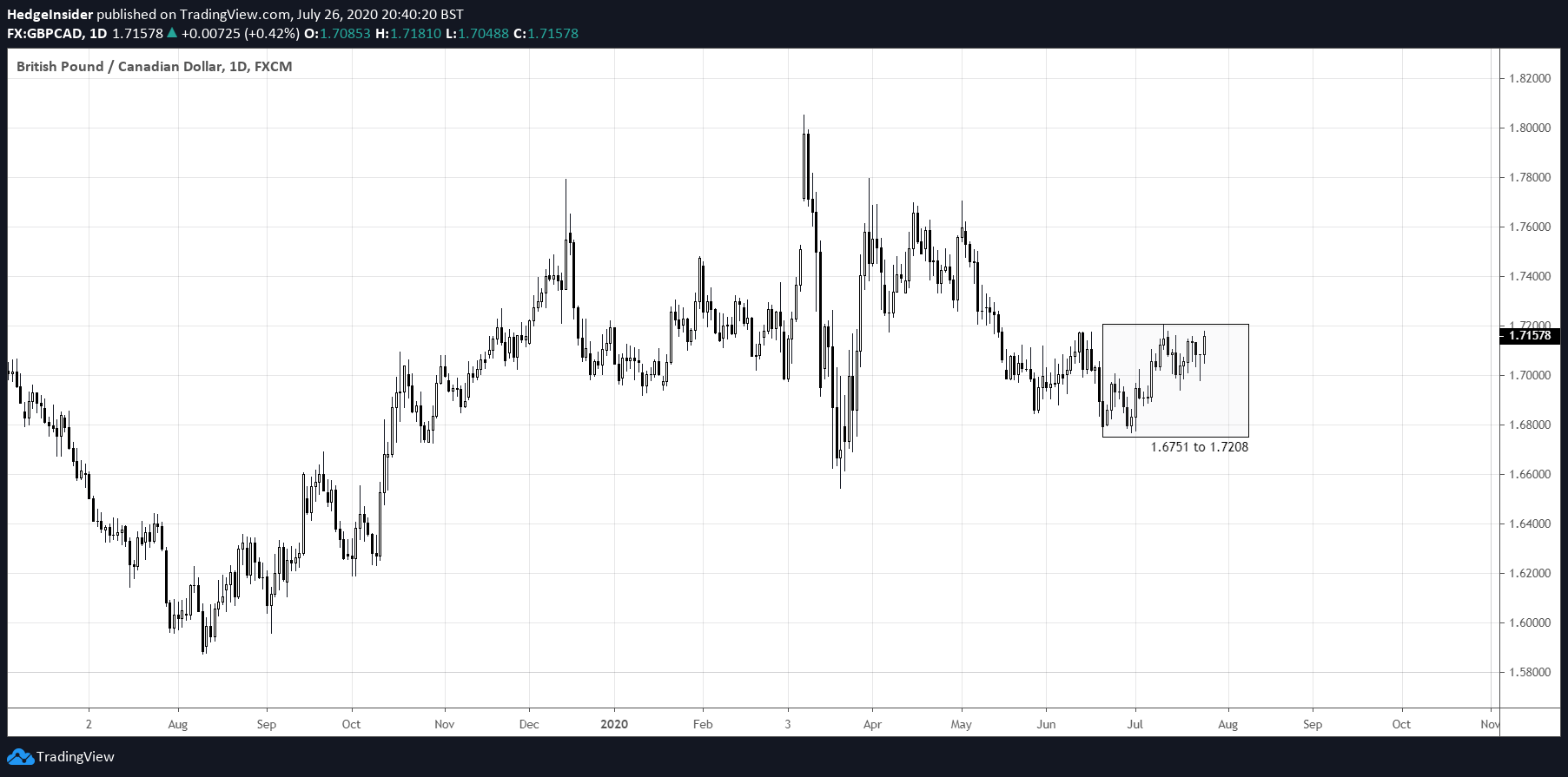

The GBP/CAD currency pair, which expresses the value of the British pound sterling in terms of the Canadian dollar, is currently trading in a relatively tight range in spite of the fact that both currencies are (at least more broadly) liable to trade with greater-than-average volatility.

(Chart created by the author using TradingView. The same applies to all subsequent candlestick charts presented hereafter.)

(Chart created by the author using TradingView. The same applies to all subsequent candlestick charts presented hereafter.)

Indeed, the fact that both currencies (GBP and CAD) are considered riskier at present is perhaps an enabler of reduced volatility, it effectively makes GBP/CAD a "risk-neutral" pair.

GBP is considered riskier for several reasons, the most obvious being that the United Kingdom has left the European Union, and the deadline for sorting out a trade deal with the EU by the end of the year remains (the country also has to arrange trade deals with a bunch of other countries outside of the EU).

CAD is considered riskier given that it is a net exporter of oil products and is considered one of the modern "commodity currencies" alongside AUD and NZD, although the latter two currencies represent countries with generally less sophisticated economies.

As the oil market has rebounded since April (when we saw negative prices for the first time on front-month WTI crude oil contracts), CAD has been able to stabilize. However, as the Bank of Canada has cut rates to the zero lower bound (or just above to +0.25%), CAD has fallen out of favor relative to its previous standing as the currency with the highest short-term rate across the G10 FX space.

There are latent risks on both sides. Although it may sound cynical, I would think it is a realistic view to take that the United Kingdom will not meet its deadline of the end of the year to sort a trade deal with the EU. (The UK had the option to request an extension to the deadline by the end of June 2020, but it decided not to take advantage of this option). Yet it is not entirely clear how badly the UK would favor in the event that a trade deal is not finalized by the end of the year; the UK would instead fall back on standard WTO (World Trade Organization) terms. Any reactive fall in GBP would boost international export competitiveness, which would provide the UK with some additional support through 2021.

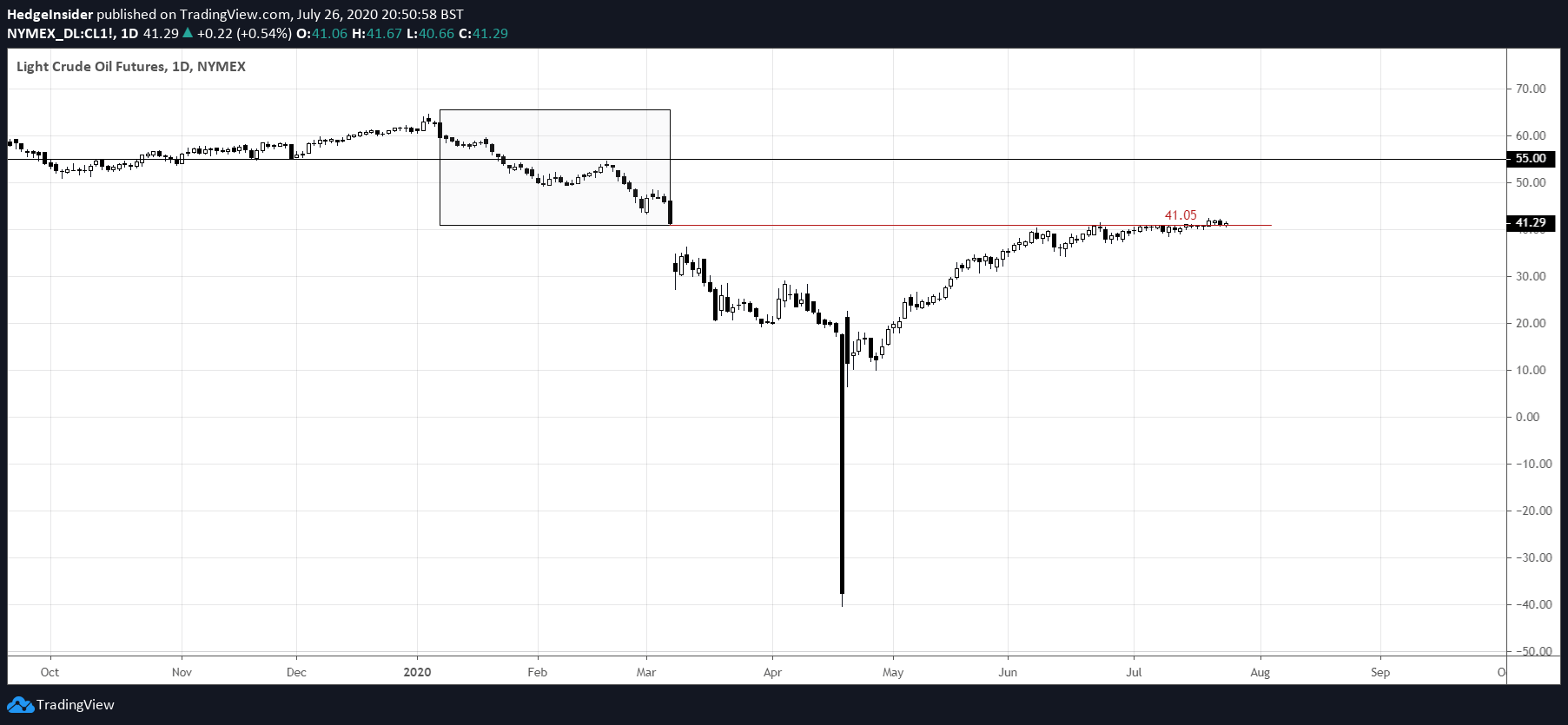

Meanwhile, COVID-19 helped to drive WTI crude oil prices into negative territory (on front-month contracts). This was given a dearth of demand (interestingly created by excess supply; buyers had nowhere to store the oil on an economically viable basis, and hence the market sought to be paid to receive the oil instead). Yet oil prices have since rebounded and remain remarkably stable in spite of ongoing uncertainties. We simply do not know where the oil market will go next, but wherever it goes, CAD will be watching.

If oil prices can hold up relatively steadily (as they currently are), this would be constructive for CAD. If we look to NYMEX WTI Crude Oil Futures, as shown in the daily candlestick chart below, we can see that the front-month contract is grinding higher but has effectively consolidated at the level that is roughly in line with the bottom of the "pre-crash" trading range at $41.05.

I would suggest this is a key price to watch for CAD buyers, as a break-down at this juncture in the oil space could quickly spill over into the FX space.

I would suggest this is a key price to watch for CAD buyers, as a break-down at this juncture in the oil space could quickly spill over into the FX space.

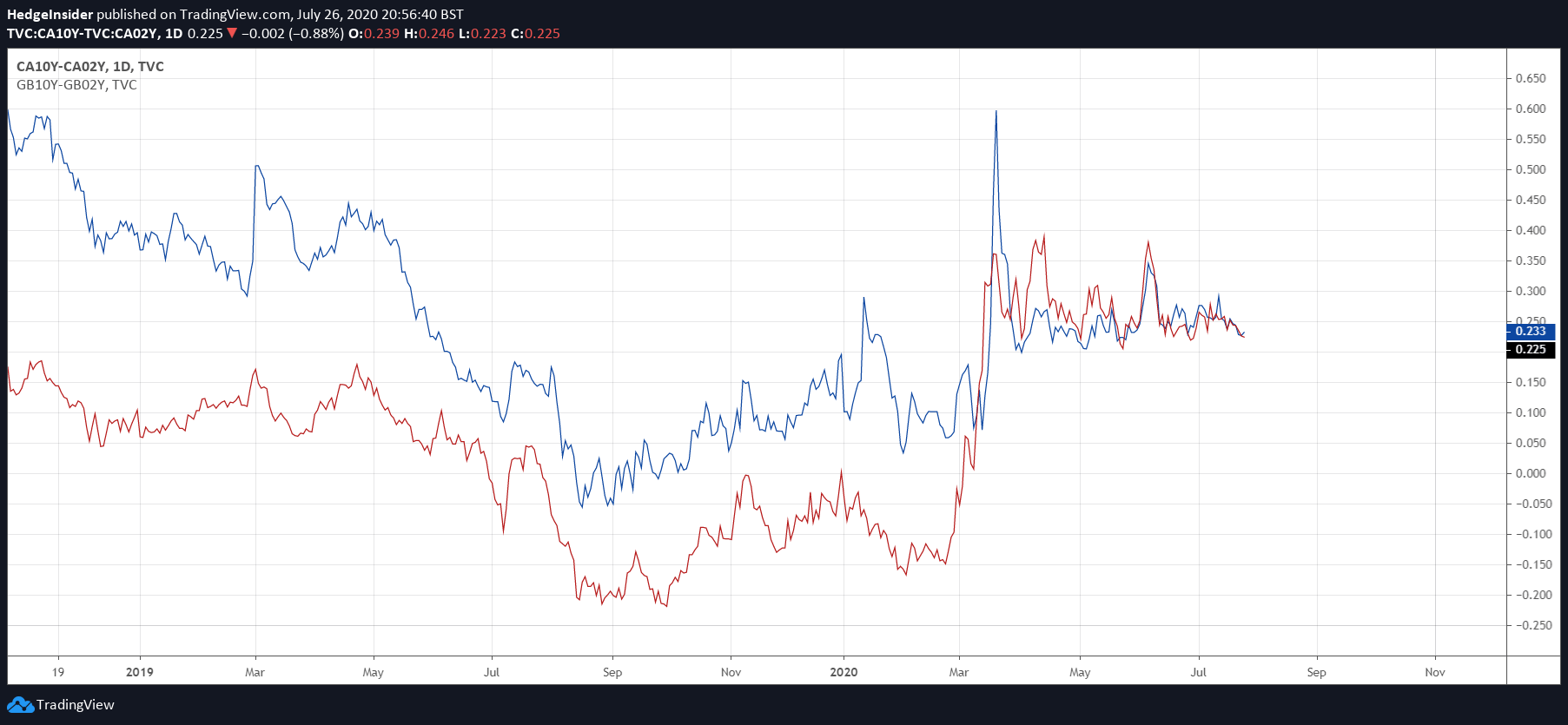

In terms of the bond market, using the 10-year, 2-year yield spread as a measure for the steepness of the UK and Canadian yield curves (presented as blue and red, respectively, in the chart below), we can see that they are practically neck and neck.

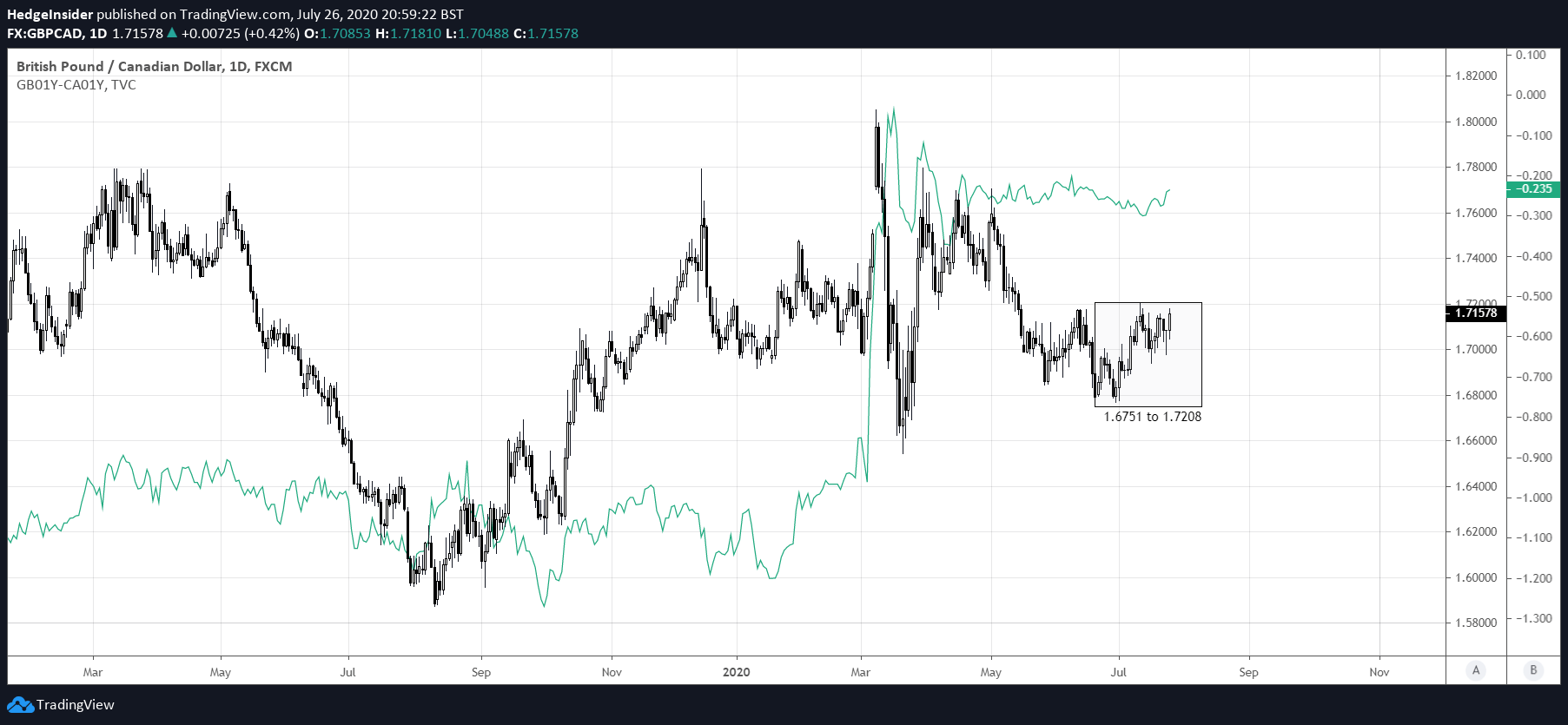

Meanwhile, we can return to the GBP/CAD chart and compare it against the short-term interest rate spread between the one-year government bond yields of these two countries (the UK and Canada). Bearing in mind that the Bank of England's short-term rate is +0.10%, and the Bank of Canada's is +0.25%, we might expect the one-year bond yield spread to be roughly -0.15% for GBP/CAD, which compares to the spread below of around -0.24%.

Meanwhile, we can return to the GBP/CAD chart and compare it against the short-term interest rate spread between the one-year government bond yields of these two countries (the UK and Canada). Bearing in mind that the Bank of England's short-term rate is +0.10%, and the Bank of Canada's is +0.25%, we might expect the one-year bond yield spread to be roughly -0.15% for GBP/CAD, which compares to the spread below of around -0.24%.

In other words, perhaps the bond market is a little pessimistic, and given that FX prices tend to correlate (and follow) bond yield spreads, I would anticipate the potential for GBP/CAD to strengthen in the near term and even test the top of its current (albeit tight) trading range of around 1.67 to 1.72. I also do not expect any interest rate changes in the medium term, from either the Bank of England nor the Bank of Canada.

In other words, perhaps the bond market is a little pessimistic, and given that FX prices tend to correlate (and follow) bond yield spreads, I would anticipate the potential for GBP/CAD to strengthen in the near term and even test the top of its current (albeit tight) trading range of around 1.67 to 1.72. I also do not expect any interest rate changes in the medium term, from either the Bank of England nor the Bank of Canada.

The world's central banks have largely coordinated their short-term rates at the zero lower bound, and given surrounding economic uncertainties, I do not expect any major central bank will wish to depart from the current common ground for the foreseeable future.

Heading into year-end, with the final Brexit deadline in close proximity, perhaps the market will view GBP risks more concretely versus CAD risks. The risk with respect to commodity prices (and commodity currencies) is at the moment based on mere conjecture; the same perhaps applies to the possible effects of a lack of a formal trade deal with the EU on the UK economy.

Yet we do at least know that the UK has a deadline coming soon, and that the market (as evidenced by past responses to trade deal headlines) seems to continue to prefer certainty over uncertainty (understandably). A lack of a trade deal presents greater uncertainty than achieving a deal, and as such, we would expect general GBP softness heading into year-end.

Therefore, the current (albeit slight) pessimism priced into the bond market may be well founded. Going forward, there is potential for GBP/CAD to retest its short-term trading range, but I continue to remain of the opinion that this pair will weaken into year-end. The level of volatility at present may be underwhelming, but the rest of the summer may change that.

風險提示:本文所述僅代表作者個人觀點,不代表 Followme 的官方立場。Followme 不對內容的準確性、完整性或可靠性作出任何保證,對於基於該內容所採取的任何行為,不承擔任何責任,除非另有書面明確說明。

暫無評論,立馬搶沙發